Slowing (fast) but Growing Bidenomics Mirage?

[embedyt] https://www.youtube.com/watch?v=LD2RRHxr-9c[/embedyt]

I’m here to break some news most on financial TV or in the media don’t know or won’t tell you. The American economy is slowing, which is normal after the consumer led holiday season, however it’s slowing pretty rapidly. As usual, Ill give you a little real time data as well as warn investors away from focusing on or even believing the short-term government data releases that so many in the media, most who have never actually managed money but rather reported on instead, seem to like to focus on.

The data is pretty clear, whether you believed in Bidenomics and the prior administrations horribly named “IRA” spending program nearing $900 billion, it provided a short term economic stimulus in 2023 and the first half of 2024 in front of the Presidential election. While grossly overstated, I’ll come back to the real data in a bit, the job market has been relatively good and stable. The unemployment rate has stayed near historic lows over the last 2 years. And while every job counts for our economy, and we would rather have more people employed than less, the types of jobs and type of employer matter greatly in the strength of the economy.

Looking at the data behind the data, you know the real data that comes out 12 to 18 months after all the revisions and government adjustments, one finds that the vast vast majority of jobs the last tow years have in in 3-4 areas that are not really private sector dependent and rather mostly subsidized by taxpayers. Th biggest job gains outside of the service travel and leisure sector have come from government hiring, education, which is also taxpayer funded, and healthcare, which for the most part is also taxpayer reliant as Medicare and Medicaid spending drive so much of our nation’s healthcare demand and costs.

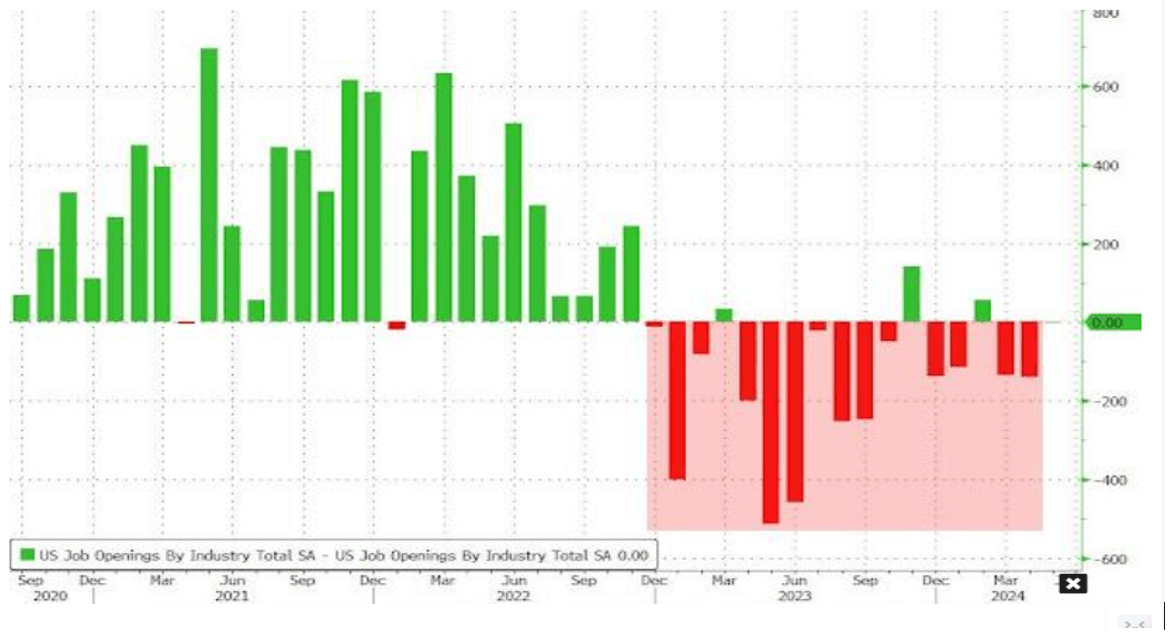

We’ve discussed for the better part of 15 months the overstatement of the strength US jobs market by the Department of Labor. Once again, we will reference the tremendous work that HEDGE Eye has done on this subject. First job openings, released in the widely discussed JOLTS report have been revised at lower 14 out of the last 17months. Here’s the chart on that weakening trend.

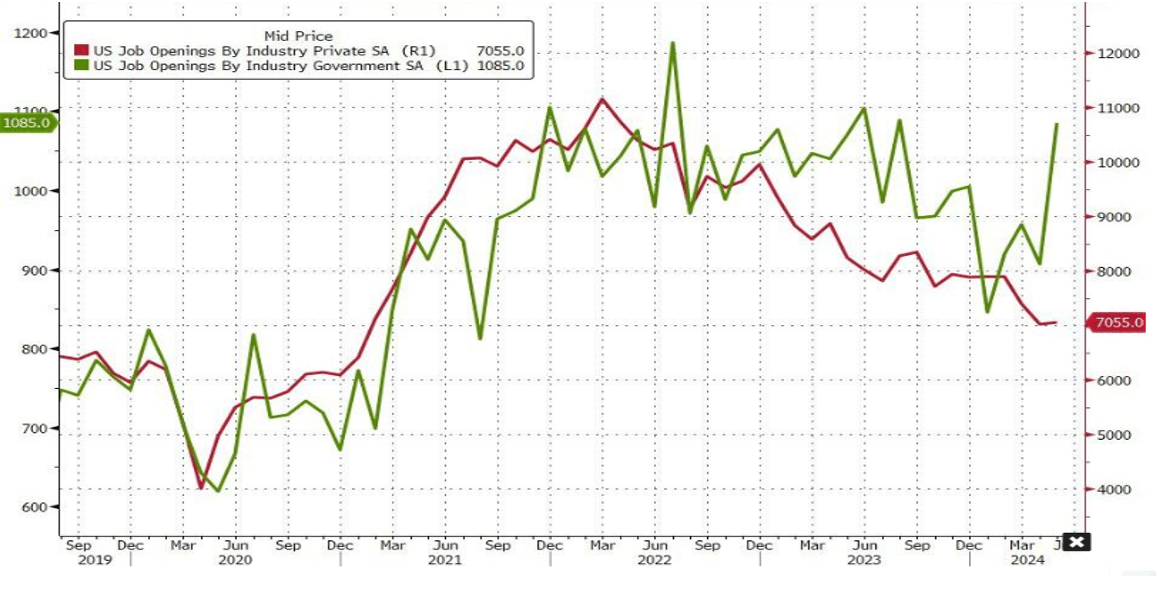

That while the short-term data, the +221k job opening increase, showed a a “beat” on? Yeap, you guessed it, government job openings, which as investors know, are taxpayer funded and create little actual long term economic output. Of the 221k increase, +179k, 81% were government openings? Really, we needed that many more government employees for what? Here’s the data of the explosion in government job openings and rapidly declining strength in private sector openings.

Over the last 3 years of the prior administrations term, the monthly payrolls revisoions have been (2022 from 441K to 380K, 2023 from 231K to 217K, 2024 from 186K to 166K), with 2024 still having more time to be revised lower. Followers know that I was no fan of Bidenomics, however as an investor, our job is to ascertain if these policies would help or hurt the economy and stocks. Our team thought, even though they were more debt fueled policies, they would help overall economic growth and earnings in 2023 and 2024 and drive stock prices materially higher as it happened.

Currently the Trump administration is looking to reverse a lot of these policies of over hiring at the Federal government level as well as allowing open borders. While I may agree with these policies in principle, an investor’s job is to determine what if any affect these might have on our economy and the markets.

Currently, the pace and randomness of the policies coming out of DC are creating huge, short-term economic uncertainty. Remember, our economy is 72-75% service and whether you or not you think our federal government is wildly overstaffed, those employees earn a wage, pay mortgages, buy food, goods and service and yes recycle these taxpayer dollars back into the economy. The rapid firing of government employees, while long-term saving taxpayers money, short term they take consumers our of the market for new purchases. At the margin they will hurt economic growth, growth that was already slowing and missing estimates due to the trailing off of the IRA fiscal impulse.

This at the same time that the new administration has changed the tariffs rules on 2 consecutive Fridays. Investors and financial markets hate policy uncertainty. Financial markets hate friction, whether caused by actual government actions like higher regulation or higher taxes or just public “brainstorming”. Investors, tariffs are friction. Financial markets hate friction. Tariffs are taxes. Financial markets and your stocks hate higher taxes. Right now whether you like the policies coming out of DC or not, the markets see those policies, be they tariffs, DOGE government employee firings, and even deportations as friction and are having a tough time digesting them as they see them all lowering economic growth and hurting, not helping revenue and earnings of most companies.

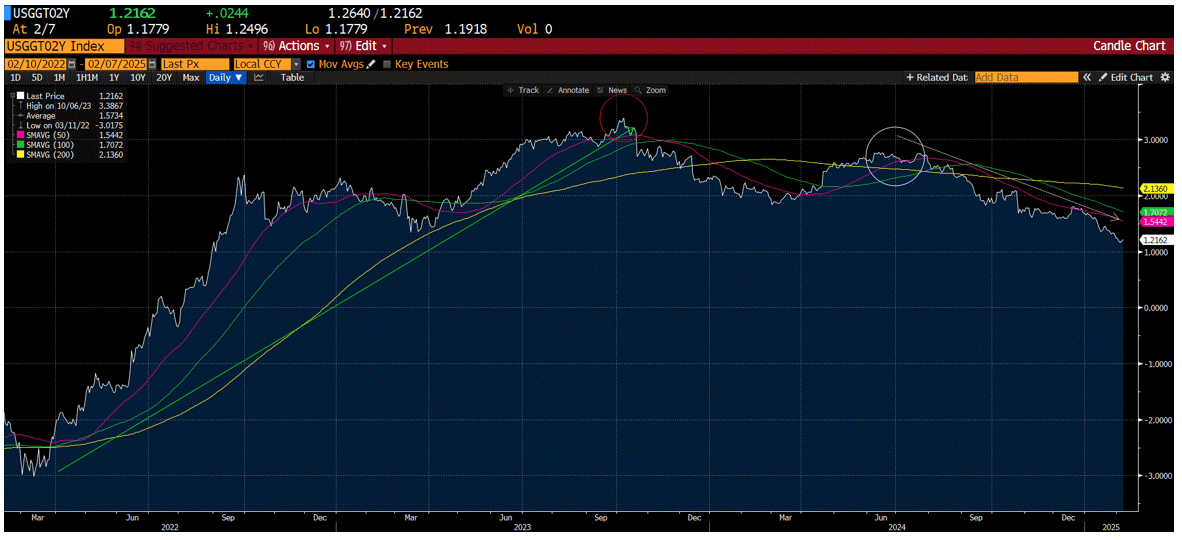

As always, where we can, we come back to real time data in the financial markets if we can find it. Long time Oak Harvest followers know I love to watch real-time real interest charts. And real-time breakeven inflation charts, the two component of nominal Treasury yields. Here’s the one for (2) year real time real interest rates. Higher from mid 2022 on the back of the fiscal stimulus of IRA spending and maybe some AI spending in the private sector, and a down and to the right, slowing trend since last summer with that downside slowing picking up since late Dec of 2024, post-election, when the concerns over policies on tariffs, government employment cutbacks, and deportations have taken center stage. Whether you like these policies or not, they are anti-growth in the short term and the bond markets see it, and the stock markets have started to wobble on their own concerns.

It’s now down and to the right, which means growing but slowing down. It means the risk of the Fed making a policy mistake by staying too tight for too long is increasing. To me, as well as the markets we are watching behind the scenes, the economic risks are not of rising inflation, but rather lower growth rates caused by 2 things. 1- the runoff of the Biden spending for 2023 and 2024 which created a bit of a sugar high, right as 2- the Trump administration implements fiscally restrictive policies like mass government firings and deportation. Remember viewers, this is not commentary on whether I agree with any of these policies or not, but rather their effect on the economy and the markets.

As we previously mentioned, soft landings in the economy do NOT guarantee no volatility. This time around, the Trump administration seem to be going for the early, “shock and awe”, which financial markets do NOT relish. They are attacking tariffs, government employment and waste, and immigration hard from the first week.

The economic surprise index is slowing and an already fragile consumer confidence due to higher inflation under Biden, is already stunting economic activity.

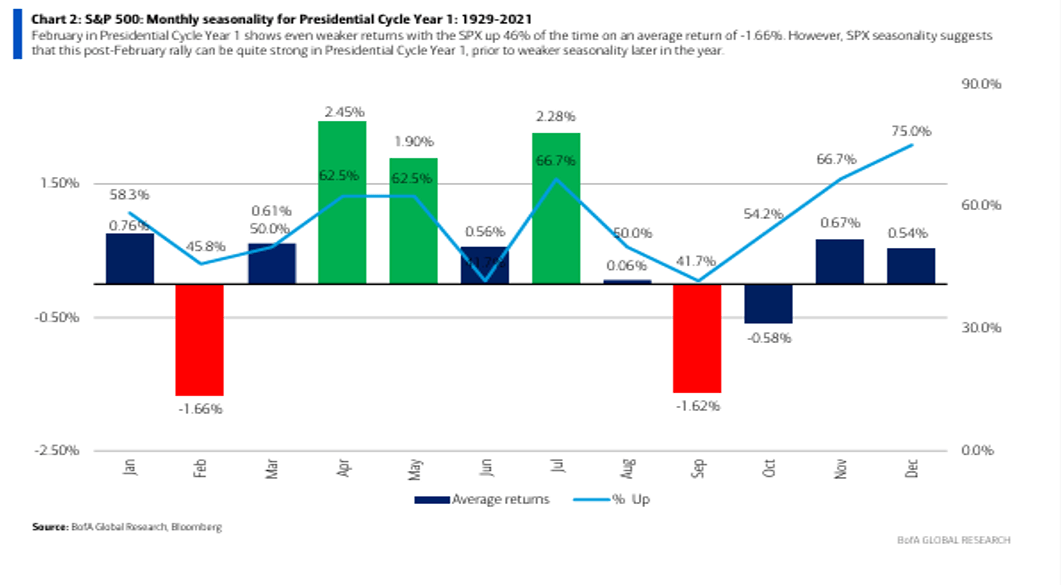

Seasonally, February does tend to be a lower return, higher volatility month for stocks, particularly the first year of a Presidential term and maybe the tariff actions and DOGE firings are this year’s excuse. I don’t know. Here’s the historic data on monthly seasonality from Suttmeier’s data group at BAC securities.

But know that regardless of the path for the economy and financial markets in 2025, the investment team at OHFG will be here manning the ship and adjusting our models and long/short hedge equity fund where we can. We expect 2025 to be a very active year for active stock management.

Until next week, have a blessed weekend.

Do you need a retirement plan that goes beyond allocating funds to truly fit your needs? We can help you create a retirement life plan customized for your retirement vision and legacy. Call us at 877-896-0040 @or fill out this form for a free consultation: https://click2retire.com/Connect

Chris Perras

CFA®, CLU®, ChFC®

Chief Investment Officer, Financial Advisor

Chris is a seasoned investment professional with over 25 years of experience working with some of the most successful money management firms in the world. Chris has made it a point in his career to adapt as the market landscape changes, seeking to utilize the appropriate investment strategy for a given market environment. His transition from managing billions of dollars at the institutional level to helping individuals and families retire is guided by a desire to see first-hand the impact he is making in the lives of clients at Oak Harvest.

Click to subscribe: